As The Tri Polar World Turns - Rolling Thunder

MACRO THEMES

If you are feeling whipsawed don't worry, it is fast becoming a normal condition. The fastest ever swing from bull market peak to bear market (16 days), the stunning weekend collapse of the OPEC + deal and Joe Biden’s amazing revival, from never winner to front runner in three weeks, it's been an insane time to be an investor. The coronavirus spread has been relentless and has now gone global as the WHO declares the first pandemic since 2009.

The effect on financial asset prices is both well-known and well documented. Things move fast in machine land - faster than policy makers can respond, leading investors to punish those who deliver too little, too late (see Pres. Trump, ECB’s Lagarde). The correlation of one within equities is back (our daily Skyview equity section - over 100 ETFs covering the globe and every sector and style - has been either all green or all red for several days). Even more worrisome is heavy selling of Gold and FI which suggests forced liquidation. It's early but the bodies are starting to pile up.

It seems clear that of the two distinct approaches to the virus - either the China contain or the S. Korean mass test model, the world has defaulted to the former, including in Europe and the US. This model comes with significant short term economic impact as the trend to experiential living gives way to stay safe mantras around the globe. The US in particular looks likely to experience weeks and weeks of burgeoning confirmed case numbers and social distancing shutdowns. The postponement of NYC’s St. Patrick's Day parade for the 1st time in its 258 year history speaks to the unique state we are in. Most importantly, the containment method may be the best way to stop the spread of the virus (once testing window is shut) but it's also the harshest method in terms of immediate economic pain & thus requires an aggressive policy driven offset. Until that offset arrives risk assets are likely to remain weak.

Global Q1 GDP will take a major China hit while Q2 will be affected by Europe and the US. Q1 US GDP is currently tracking positive with Atlanta Fed Nowcast as of March 6th at 3.1% and Blue Chip Consensus at 1.4%. Policy action is needed now to save the 2H as Bloomberg’s US recession indicator blows past 50. The gold standard would be aggressive health measures (starting to get) and offsetting coordinated global fiscal stimulus, yet that standard is unlikely to be met as one recalls that both the G-7 and G-20 have met since the virus became known and yet both groups did absolutely nothing. We expect instead a “rolling thunder” of policy responses from different countries as each country deals with things on their own, perhaps with monetary & fiscal policy makers of the same country working together as has occurred in England.

Will it be enough? Time will tell. Financial markets have made it very clear to policy makers that they must go fast & go big. The problem is that going big and fast in containment means a big, immediate economic hit which then requires a similar sized policy response, which is lacking to date. The worst equity day since 1987 does seem to have finally spurred policy makers with the US House close to a fiscal package and both Germany and the EC adopting max flexibility in fiscal rules.

We are watching Four Issues: peak caseloads in Europe & the US ( when China case load rolled over its equities started to advance), the US - EU policy response, consumer confidence & job numbers, investor positioning/sentiment coupled with cheap markets (US equity still not there - ROW is). The shift from a health issue to an economic issue has occurred - now policy makers need to ensure it doesn't morph into a financial market meltdown. Containment both in health & wealth terms.

ECONOMICS

We are in a data vacuum - any pre virus data is almost immediately discounted. The global economy was picking up into the virus outbreak but what lies on the other side is hard to tell. China’s Feb PMI numbers were staggeringly bad - Italy’s total shutdown implies similar data points ahead there, at least for the next few months. The US response remains haphazard & incomplete, suggesting similar shutdown efforts & attendant economic impact may be required here as well. The V that some, including us to be fair, expected has now been pushed out to the 2H if we are lucky. This brings to mind the famous Clint Eastwood line in Dirty Harry: “Do I feel lucky? Well do ya, punk?” As he stares down the barrel of a Colt 44.

One major concern is the impact on the service sector which social distancing and containment/quarantine, self-imposed or otherwise, will have on a segment that represents 65-75% of most developed economies. Our 2019 call for a Lower for Longer Global Growth path was underpinned by record low UER and above inflation wage gains which suggested the consumer was fine and would support DM economies during a manufacturing slowdown. This can no longer be assumed, at least in the near term. This is especially the case given the absolute body blow that will be suffered by all involved in the experiential living side of the economy which is to say virtually everyone employed in serving other people. The rapidly dwindling Manhattan lunch crowds are just one anecdotal indicator.

In addition, the rebound of the Chinese economy, now officially underway as Pres. Xi visits Wuhan, is likely to be negatively affected by the slowdown outside of China and thus the inventory rebuild and refilling of supply chains may not be as robust as one thought even one or two weeks ago. The ebb and flow of the interconnected global economy means one has to constantly think about how one part might affect another - the virus & Govt response (US shutting off air travel from Europe for a month) seems intent on calling global connectivity into question, something we have noted in our Tri Polar World work.

Bottom line: global growth is likely to be flat to down from last year, depending on virus spread and the rolling thunder response of various Govt stimulus efforts. It seems that short term sacrifice, ie a quarter or so of weak/no growth is inevitable; the hope must be that it leads to a more robust and sustained 2H rebound. The V recovery remains alive but it might come from a lower than expected trough.

POLITICS

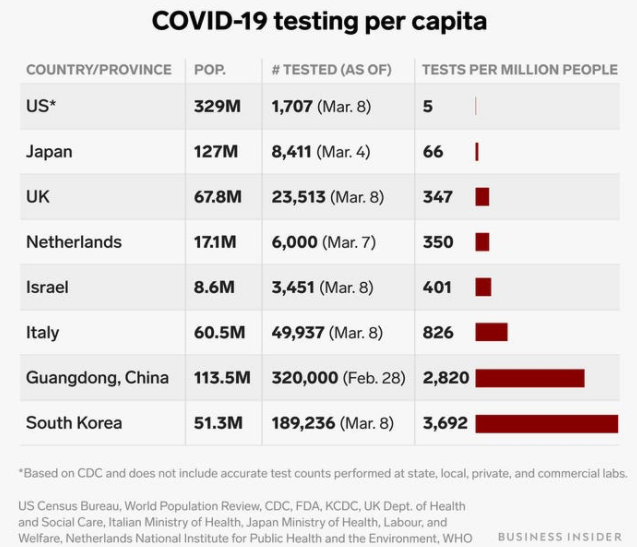

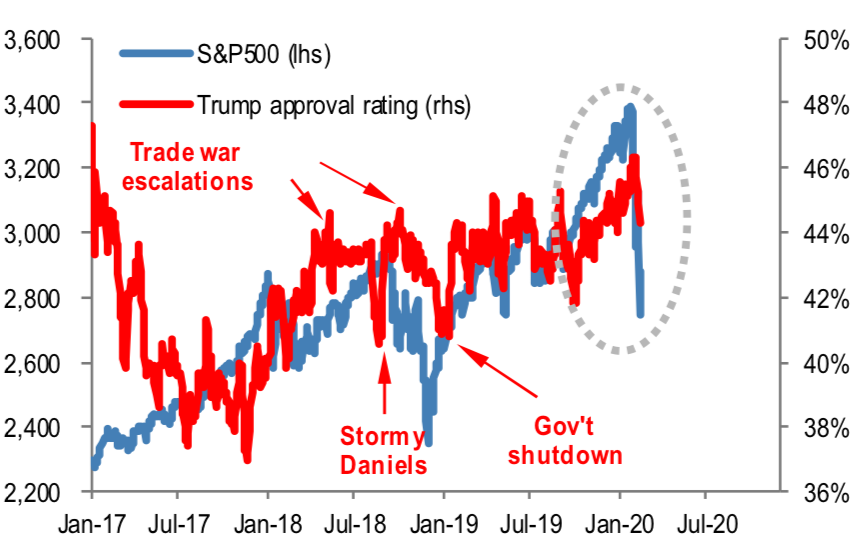

The virus may scramble quite a few political calculations before it is done. In the US, Pres. Trump’s re-election prospects have taken a major hit, as his March 11th prime time address to the nation fell completely flat. History suggests that Govts don't get credit for doing the right thing but definitely do get the blame for doing the wrong thing. So far, the administration's response to the virus has been subpar at best as Chart 1 shows. The chaotic nature of the response, the downplaying of the risks by the President himself suggest the height of ironies may be upon us: that Pres. Trump, a famed germaphobe, may be brought down by a virus. As President, Trump has never been in as much trouble as he is today: virus outbreaks, sports shutdowns, bear markets and recession are not supportive of re-election. (See Chart 2)

Chart 1: US Testing is a National Disgrace

Source: Skye Gould, Business Insider

Chart 2: The Virus Could Bring Down the President

Source: JPM

In addition there is the miracle in South Carolina that led to Joe Biden’s resuscitation. Biden, who as a presidential candidate had never won a primary in his multiple runs for the Presidency, has now dominated the field in the past few weeks, taking a commanding lead over Bernie Sanders. This too suggests trouble for the President who might find his Ukraine attacks gain little traction in a cooped up electorate while Biden develops a broad coalition of supporters across race, class and gender to take on the President.

Elsewhere President Xi’s Wuhan victory lap suggests that after some initial delay and trouble the CCP will be found to have handled this virus quite well, particularly in comparison to the West. It's quite clear that those countries that recognized the problem and got on it fast: S Korea, Singapore, China once past the initial delays, have coped much better than those who delayed and obfuscated such as Iran and Italy. Sadly the US is following much closer to the latter path than the former.

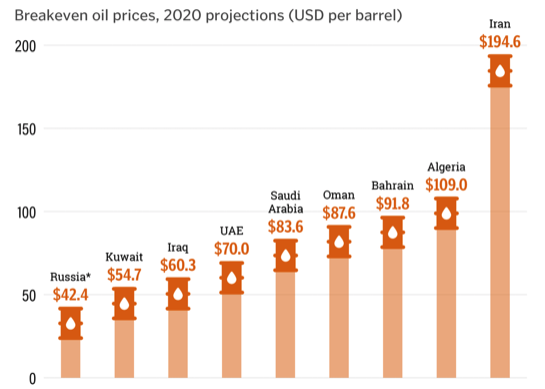

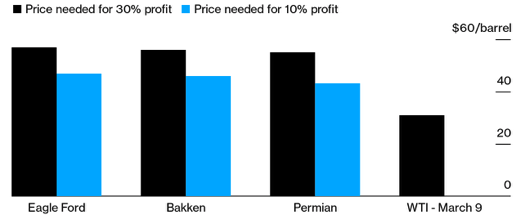

Finally it's worth noting that Russian President Putin seems to have managed an impressive two for one shot with his decision to not support an additional OPEC + production cut. This has led Saudi Arabia to pump as much as possible over the coming months, offer large discounts to European markets that Russia normally supplies and in general unleash an all-out oil war into a market that faces rapidly shrinking demand, which in turn could result in the collapse of much of the US shale oil patch. As Chart 3 suggests Russia is much better placed that SA to deal with a sub $40 oil price while Chart 4 lays out that much of US shale production is uneconomic at current price levels. With Prince MBS having arrested his uncle and numerous others, it is hard to see a Saudi climb down any time soon.

Chart 3: Russia Better Prepared for Oil War than Saudi Arabia

Source: IMF, Bloomberg

Chart 4: Putin Takes Aim at US Shale

Source: RS Energy, Bloomberg

POLICY

This where the rubber meets the road. Policy response to the virus needs to incorporate health, fiscal and monetary efforts across virtually all nations at this point. Policy makers seem outclassed by the spread of the virus & the (machine assisted) speed of the market discounting process; the IMF did announce an aid package to EM a few weeks ago but that has been the extent of global cooperation. It's hard to see how this will change given isolationist US leadership, new and untested EC leadership, an increasingly isolated Angela Merkel and the Asian triumvirate of Xi, Abe and Modi each marching to their own drummer.

We will have continued dollops of policy action; the Fed two weeks ago, last week from the RBA and others, this week’s twin UK salvo, the disappointing ECB meeting and next week the Fed again (markets pricing 75-100bp cut). Tightening financial conditions would seem to require more Fed action (See Chart 5). The Fed’s massive, $1.5T liquidity injection is both comforting & scary leading one to wonder what lurks beneath? The PBOC has been relatively quiet with some suggesting it (and the rest of the China policy team) wants to wait to see how the return to work goes as well as how weak the Q1 data will be before announcing stimulus. Given that China has been responsible for roughly 30% + of recent global growth, delay there is worrisome.

Chart 5: US Financial Conditions Require Fed Action

Source: Bloomberg

The DM's failure to utilize fiscal policy is baffling. Governments can borrow at zero or just above/below; climate change is a real and urgent problem that can absorb lots of Govt money; the German CA surplus is roughly 7% of GDP, its infrastructure is in rapid decline, its approach to technology antiquated and yet the call is to stick to a balanced budget. In the US the Govt’s failure to produce a fiscal plan weeks and weeks after it became clear the virus would hit the US is baffling - if for no other reason than President Trump’s re-election likely depends on it. Potential next moves include Pres. Trump declaring a National State of Emergency and/or a large fiscal package put together by the House and accepted by Senate Republicans & the President given how he fell flat in his address.

As Bloomberg’s Jon Ferro pointed out to me on air the other day, when I was arguing that the current Trump Admin is filled with small Govt folks who don't want to spend money, the US budget deficit is over 5% of GDP - well played Jon and absolutely correct. But in this instance there seems to be a slow motion walk to the door which of course brings to mind the Grateful Dead classic song Fire on the Mountain: Studio. Extended (better)

''Long distance runner what you standing there for?

Get up, get out, get out of the door….

Almost ablaze still you don't feel the heat…

Long distance runner, what you holding out for?

Caught in slow motion in a dash to the door”

Well there is a virus burning through the US and the lack of meaningful Govt response has already ended the longest bull market in US history.

MARKETS

The old adage that markets hate uncertainty has rarely rung more true; today we need to add that machines on the other hand don't know uncertainty and they seem to be in charge. Lots of questions, few answers. Should one sell equities at 2500? Are long duration bonds still a buy? How much room is there for credit spreads to widen further? Are commodities oversold enough to start building a position? How come gold has been weak of late? Is the VIX volatility storm over?

If one sells here and goes to cash he/she might feel very good for the next one to two weeks, maybe months but quite likely not quarters - will one be smart/lucky enough to know when to buy back in? What's the right EPS number for the US, Europe, Japan? Clearly not the one still showing which suggests if anything analysts have taken Q1 down and added to Q4. Expect EPS adjustments en masse once Q1 reporting season kicks in. The frothy bull nature of markets just a short month ago is long gone as Chart 6 suggests.

Chart 6: Sentiment/Positioning Getting Better

Source: JPM, HFR

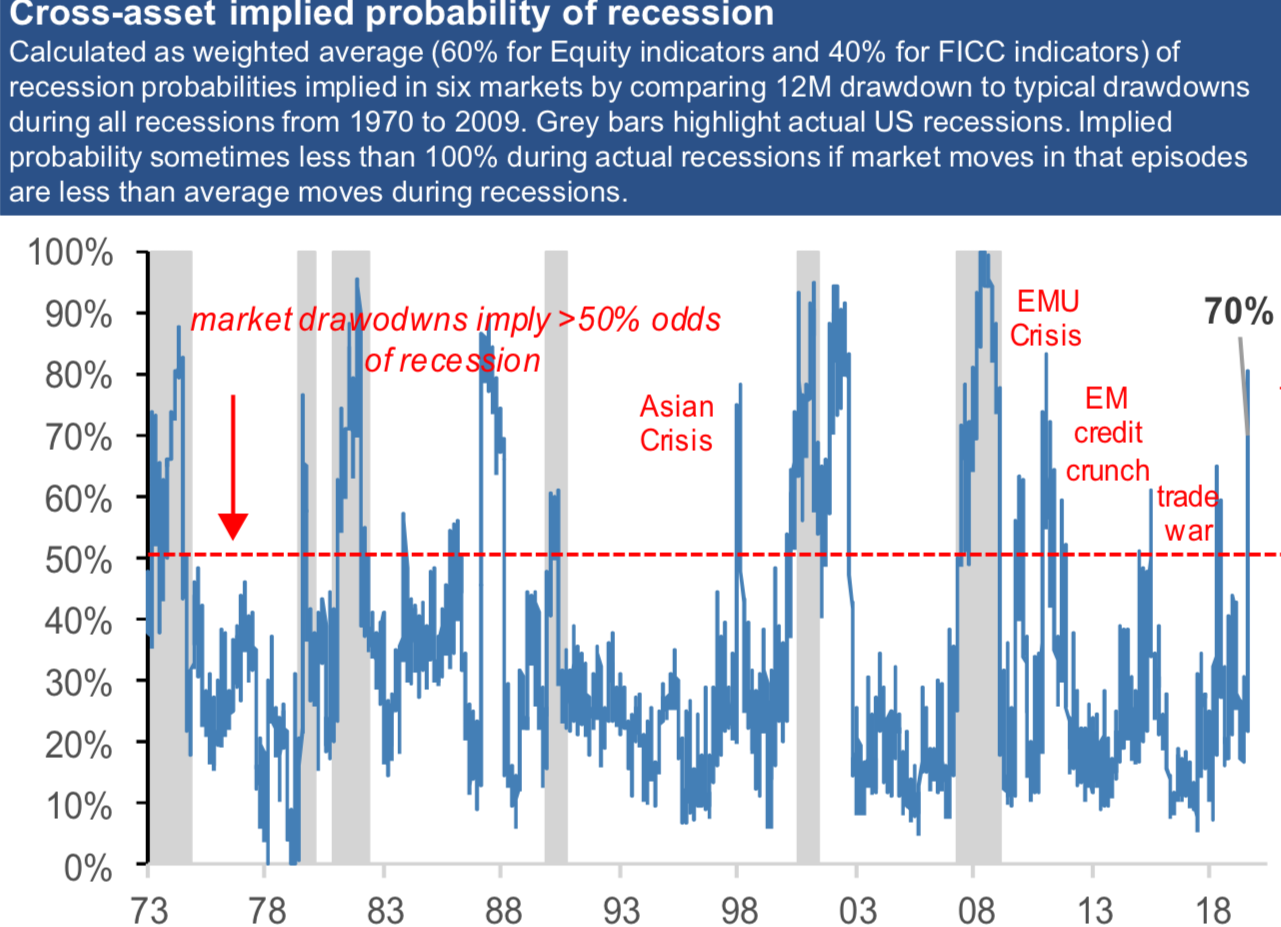

Entering 2020, the playbook coming was about global growth rebound, Relation 2020 as Central Banks let inflation run hot, rates backing up and Value/Cyclical segments of the market finally having their day in the sun. All that has been reversed in some pretty brutal fashion. Now global growth will take a hit - our Lower for Longer Global Growth Path is at risk to containment and quarantine measures (as I write the ALL sporting events in the US including March Madness, NBA, NHL, MLB, and even the Masters have been canceled/postponed). Instead of talking about inflation we are talking oil price collapse and a deflationary risk profile. The volatility storm (VIX hit 77 as we write, ATH was 80 in 2008) is leading to massive deleveraging and waves of selling into illiquid markets. Value and cyclicals have been taken to the cleaners yet again. Fear and greed indicators have flat lined on Fear, suggesting sentiment can't get much worse while assets have gone a long way to pricing in recession. (See Chart 7)

Chart 7: Risk Assets Pricing in Recession

Source: JPM

In Fixed Income, the long duration UST rally has been a mega home run but now what? The bigger the virus the bigger the policy response and the more risk duration offers rather than reward. The UST yield curve is now steeper than its been in months. Credit spreads have blown out, especially in the energy space and there is talk of levered multi asset and credit funds who, unable to stomach the negative yields on offer in European Sovereigns, came to the US credit market and are now stuck with gross exposure levels that suggest more selling ahead. Such selling could migrate to the equity space given liquidity still exists there, unlike in credit. AGG and GLD are both down substantially which is very worrisome. The next few weeks into Q end is a time to tread very carefully in credit.

In Alts the commodity space has been hammered led by oil down 30%+ in a matter of days...it’s been a breaking record run across assets but especially in the commodity space. Gold has been the standout but recently it's been acting poorly reflecting perhaps some forced selling? Dr. Copper has been valiantly trying to hold its early Feb low - could it be the canary that says global growth will make it through this ok? Targeted stimulus would not seem like a buy signal for industrial metals though it's clearly been in the crosshairs for a while now which suggests selling might be pretty washed out.

Hard to say buy the oil patch here given what would seem to be further weak demand ahead as the US and Europe slow while SA and Russia pump. Lower prices would seem to lie ahead - at least back to 2016 levels of roughly $27 on Brent. (See Chart 8)

Chart 8: Is There An Oil Slick Ahead?

Source: JPM

The public markets now look to the private markets for some support as PE has gobs of dry powder available to be put to work. However, given that many banks and large funds are dispersing their people and not letting folks on planes it's hard to see a ton of deal flow happening in the near term. Drawing down credit lines is already under way led by Boeing - more are sure to follow. Until folks can get back on planes and meet face to face the IB part of the big banks seems likely to suck wind.

At this point, down roughly 25-30% across the equity space with only China bucking the storm, interestingly enough, the question is buy, sell or hold? Selling now locks in losses that will be hard to recoup. Cross asset action suggests we are getting close to an end game with gold and bonds, both having held up well, now selling off aggressively, suggesting a true flight to cash. A lot depends on time frame - if short term sell on up days, if medium to long term look to scale in on down days with the view that six months from now things will look much better from a health, social and economic POV. Comparisons to 2008 - 9 seem overblown with the financial system in much better shape, leverage dispersed through the system, few obvious imbalances, the global economy coming in to this in decent shape, US housing in great shape, Govts free to borrow at generational low rates etc.

Fiscal action is needed which suggests duration carries a lot of risk, energy patch and leisure, travel etc suggest default risk in credit. EM dollar debt has been hard hit & remains attractive. Of the alts space, waiting for other shoe to drop in energy seems to make sense while metals might be worth looking into as the scale and scope of fiscal stimulus becomes clearer. One could do worse than syncing up sizing/quality concerns via stimulus size.

One question to ponder is whether this bear market sudden and fierce as it is will be sufficient to reset the equity market leadership table both geographically and sector/factor wise. The US with its Growth component has been the leader since the GFC low 11 years ago this week. Today the US remains expensive even after a 25% decline - this is a problem. Or will it be more like 1998, a violent sell off that once markets resumed moving up returned to the same tech leadership which lasted until two years later and the tech meltdown of 2000? When you are sick of thinking about the coronavirus and afraid to go home to your self-quarantined family, think about this question. What's happened has happened - it's what happens next that counts.

PORTFOLIO STRATEGY AND ASSET ALLOCATION (GMMA)

We have adjusted our portfolios to reflect the growing uncertainty around both growth and earnings. We have reduced risk across the board: Equities, Credit & Commodities and raised cash. At this point US equities are not yet cheap, Credit is impaired, UST are overbought and Commodities have been left behind. We have reduced our Value and Cyclical tilts as part of this process as well.

Within Fixed Income we note the steepening of the US yield curve in anticipation of significant fiscal response and remain concerned about the oil crash impact on the Credit side. Should the fiscal response be aggressive and the economic hit be only a quarter inflation could surprise to the upside. EM $ debt has been taken to the cleaners - we remain invested.

Like several assets, FX has gone from an ATL in vol terms to gyrating significantly both in EM and EM FX. EM FX has held in better than expected given the action elsewhere.

In the Alts space, our recent add to Commodities proved ill-timed and we have reversed that decision. Energy would seem to have further downside while industrial metals have demonstrated relative stability vs growth fears - we are watching with a close eye.

GLOBAL MACRO SUITE PORTFOLIO CHANGES

Global Macro Multi Asset (GMMA)

Within our Equity holdings we reduced our Value & Cyclical positions while adding to our Growth & Technology positions. We also reduced our EM equity positions.

In our Alts sleeve, we exited our broad Commodity and Silver positions while adding a Gold and Energy related position.

We built a Cash position.

Global Macro Income (GMI)

We exited our EU HY position, switched our Equity Value to Global Min Vol and our Silver position to Gold. We also built up our Cash position.

Global Macro Equity (GME)

We exited our Min Vol position and switched our Broad Commodity position to an Energy focused position

I hope you find this monthly piece of value and look forward to engaging with you on a monthly basis as we move through 2020.

Jay Pelosky, CIO & Co-Founder

TPW Investment Management

DISCLOSURE:

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. Returns can vary dramatically in separately managed accounts as such factors as point of entry, style range and varying execution costs at different broker/dealers can play a role. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts are inherently limited and should not be relied upon as an indicator of future results. There is no guarantee that these investment strategies will work under all market conditions, and each advisor should evaluate their ability to invest client funds for the long-term, especially during periods of downturn in the market. Some products/services may not be offered at certain broker/dealer firms.

There can be no assurance that the purchase of the securities in this portfolio will be profitable, either individually or in the aggregate, or that such purchases will be more profitable than alternative investments. Investment in any TPWIM Portfolios, or any other investment or investment strategy involves risk, including the loss of principal; and there is no guarantee that investment in TPWIM’s Portfolios, or any other investment strategy will be profitable for a client’s or prospective client’s portfolio. Investments in TPWIM’s Portfolios, or any other investment or investment strategy, are not deposits of a bank, savings and loan or credit union; are not issued by, guaranteed by, or obligations of a bank, savings and loan, or credit union; and are not insured or guaranteed by the FDIC, SIPC, NCUSIF or any other agency.

The investment descriptions and other information contained in this are based on data calculated by TPW Investment Management, LLC (TPWIM) and other sources including Bloomberg. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. This report should be read in conjunction with TPWIM’s Form ADV Part 2A and Client Service Agreement, all of which should be requested and carefully reviewed prior to investing.