As The Tri Polar World Turns - September 2019

MACRO THEMES

Markets chopped a lot of wood in August. The obligatory EM collapse in Argentina, ugly tit for tat tariff hikes in the US-China trade conflict which led to the RMB cracking 7 and the long awaited crossing of the Rubicon of US Yield Curve inversion between the 2-10 yr UST rates. These events also served to further extend the already very stretched factor positioning across Growth/Momentum & Value. Along the way anything with Cyclical exposure was thrown out with the trash. Late in the month, Bob Marley’s song Survival echoed in my ears as I feverishly hit the gym to stave off fatigue and angst… August in Manhattan - hot time in the city.

Two weeks later & here we are - September, the start of Fall and there is a new song on the turntable: Bob’s Wake Up and Live as opportunity seems to be brewing for a significant Fall risk asset rally. Below are several reasons why:

What doesn't kill one makes one stronger and risk assets survived August

Positioning is very offsides with hedge funds at 2008 levels of exposure

Sentiment is horrible with indicators pointing to levels not seen since the March 2009 lows; Seasonality improves as we head into Fall

Central Banks are in a Global Easing Cycle with over 80% easing

The Global PMI just had its first increase in 16 months - tends to occur 4 months before end of global slowdowns

Last but far from least, technicals are better & stocks are very cheap relative to massively overbought bonds

While an impressive list, risk assets still need a catalyst to move higher.

One such catalyst could be a 2019 trade deal between the US and China, just as everyone has kicked such a prospect into 2020. The language and tone from China is better, including phrases like “meaningful progress” while both sides have offered goodwill gestures over the past few days. China’s bid to narrow the focus of the October talks is bullish for a deal while in the US it's all about what best helps the president's reelection prospects. Slipping poll numbers and a decelerating economy suggest a deal BEFORE year end that would help 2020 C-suite capex planning & reduce recession risk. Across the pond, the prospects for a Brexit deal are improving after Boris Johnson’s awfully bad, horrible few weeks as PM. Peace in our time on both sides of the Atlantic could catapult risk assets higher. We are focused on equity exposure particularly to non US, Cyclical and Value segments of the markets.

ECONOMICS

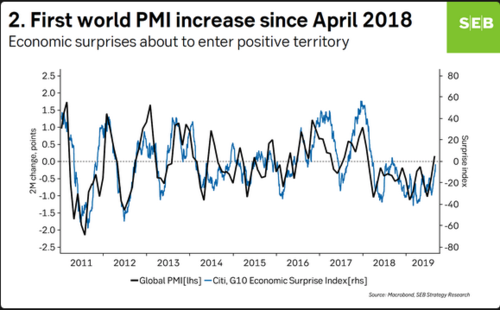

As part of our Lower for Longer Global Growth Path theme we have consistently highlighted the importance of & difference between the Service/Composite PMIs and the Manufacturing PMIs. This distinction continues as Service PMIs came in better than expected in Europe, Japan and the US signalling continued low growth boosted by the twin positives of record low unemployment and rising wages across the developed economies. While the US Manufacturing PMI just broke below 50, global manufacturing PMIs have been in a downturn trend for well over a year, the longest such decline since 2012. We believe the US “catch down” is more likely to signal the end of the global manufacturing slowdown than the beginning. The EM Manufacturing PMI for example has already hooked up while there are growing signs of stabilization in Europe’s manufacturing sector. (See Chart 1)

Chart 1: Global Growth Bottom Ahead?

Source: SEB

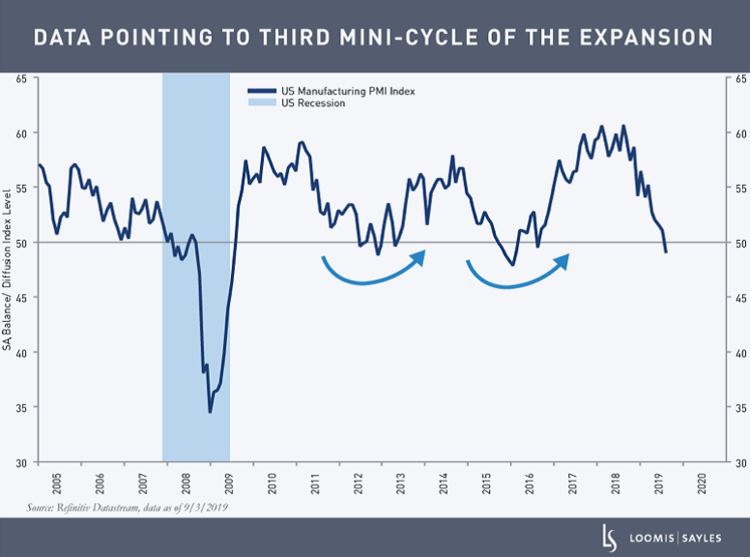

US recession risk remains quite limited: for example, Ned Davis Research’s (NDR) 10 US recession indicators shows only one flashing red (CEO confidence). The yield curve inversion, while already reversed, has allowed folks to note that it is an imperfect signal especially in a low rate world and one that implies anywhere from 16-20 months before a recession. The US also benefits from the growing pile of negative yielding debt as the ability of US corporates to borrow at lower and lower rate levels should reduce the risk of a credit crunch and help extend the economic cycle. This suggests a mini cycle is more likely than a recession as Chart 2 illustrates.

Chart 2: US Mini Cycle, Not Recession

Source: Loomis Sayles

Perhaps most interesting on the global economic front is the growing recognition that China is unlikely to massively stimulate its economy and instead is ok with an L shaped recovery (hat tip to my former Morgan Stanley colleague Stephen Jen). This economic stance allows China to demonstrate resolve in its trade conflict with the US while controlling its own macro economic destiny. Perhaps more importantly given China’s role as the global economy’s principal growth engine over the past decade it makes clear that we are in a global regime change where China will neither sink nor save the global economy.

This has multiple important ramifications. Viewed from the Tri Polar World framework, it reinforces our sense that each region will increasingly be required to self stimulate or generate its own demand thus furthering regional integration. China’s L shaped recovery also shines a spotlight on Europe in general and Germany in particular as free riders on global demand. Financial markets, ahead as usual, have been repricing much of corporate Germany to reflect this new state of affairs.

While Europe does indeed have a heavy trade dependency (Chart 3) it also has a new European Commission which seems well aware of this need. Developing a new internal demand framework which includes fiscal policy is an urgent task for Europe; such a framework will be key to maintaining European & global growth in the years ahead. The penny (pfennig) is even dropping in Germany itself as calls grow for fiscal stimulus.

Chart 3: Europe Needs to Develop Internal Demand

Source: KKR

The likelihood of some additional spending in Germany seems quite high as pressure grows from both the business and banking lobbies. Germany’s Green energy plan is due in September and could be fiscal stimulus’s Trojan Horse. The cost of negative rates to the banking community is increasingly recognized while the Industrial lobby is pushing hard for the state to help replace demand lost to the industrial slowdown by boosting infrastructure & green energy projects, taking advantage of record low rates to stimulate both near and long term growth.

In Asia, China seems intent on micro dosing stimulus via both monetary and fiscal policy while better than expected growth in Japan has meant that the upcoming VAT hike is likewise being offset by small bore stimulus policy. Elsewhere, it is increasingly clear that economies will need to stimulate for themselves using both fiscal and monetary policy measures. In Asia, Thailand and India have both announced fiscal stimulus programs while in LatAm rate cutting continues with both Mexico & Brazil reducing rates. Weak growth in both suggests rate cuts are likely to continue.

POLITICS

August suggests that the idea that Trump would be bombastic on the campaign trail and quiet on the world stage should have come with the caveat that the trade front is its own animal. Now in September it seems that a more deal making President is ascendant, firing his National Security Advisor and suggesting open ended talks with Iran & North Korea while his subordinates massage a better tone with China. Perhaps the chaos in August even wore out the president - more likely is the clarity provided by an upcoming electoral calendar coupled with declining poll numbers.

The weaker the US economy, the worse the polling numbers & the greater the need for the President to make a deal. The time could be right after the Fed’s September meeting and China’s 70th anniversary on Oct 1st to make a China deal happen.

While a hard Brexit remains a real risk in Europe the debacle of the past few weeks could serve to open the way for a Brexit deal - again something that investors have virtually given up on. Boris Johnson’s loss of majority could free him up to be more flexible on the Irish backstop question while Europe’s new leadership, led by Ursula von der Leyen, may also be more flexible.

Europe’s new team reflects Europe’s breadth and depth across both gender and geography. Of particular interest is the retaining of Denmark’s Margrethe Vestager as both antitrust and digital economy commissioner - marrying the two suggest Europe gets that the digital world is fast overcoming the physical world and that data not manufactured goods are what needs to be measured and measured well. From our Tri Polar perch we can do little but quote from the FT’s editorial page: “Ms von der Leyen and her team have begun to map out Europe’s place between the US and Chinese behemoths: a regulatory superpower that can protect and project its model of a sustainable social market economy”. The Tri Polar World is manifesting itself right before our eyes.

One would be remiss by failing to note the amazing own goal scored by Italy’s Salvini - recall how just 3-4 months ago he was about to bestride Europe as the populist standard bearer - now he is out of Govt as Italy seeks to stabilize its economy and its relations with Europe. As new European leaders take their places the hope must be that fiscal stimulus becomes a part of the game plan - rates are at generational lows and needs exist everywhere, what's been lacking is the political will.

POLICY

While both Jackson Hole and the G 7 meeting disappointed, there are a number of positive factors at work. Central Banks are in a full blown global easing cycle with over 30 cuts to date and an anticipated 50-60 more in the coming year. The Fed will cut next week and perhaps one more time before going quiet in the 2020 election run up. Liquidity is expanding with US MS figure showing a sharp increase in the past few months. The ECB has joined the party with Mario Draghi’s swan song likely to help stave off recession while his successor Ms. Lagarde is likely to try and bring both monetary AND fiscal policy to bear in Europe. China’s PBOC meets soon after the Fed and is likely to continue its monetary easing efforts as well.

September also brings the OPEC+ meeting which is likely to include further efforts to stabilize and even boost oil prices given Saudi needs and desires to float Aramco and continue its domestic growth program. A full blown global easing cycle, growing willingness to use fiscal policy in Europe and Asia, efforts to boost oil prices all coupled with likely tariff driven US inflation suggests that the duration bulls should be careful not to consign inflation to the dustbin of history. August core US CPI came in at 2.4% y/y, the fastest since 2008, increasing the likelihood that the Fed is likely to ease one or two more times rather than engage in a full blown easing cycle.

Our Lower for Longer Global Growth Path remains a useful construct though perhaps with a more elongated and subtle pick up in elevation. Our Big Four signposts remain useful: Global Easing is aggressive and should soon begin to have an effect. The Trade front has been worse than expected but seems to be setting up for a positive surprise; a Global Growth bottom may be approaching as might be a bottom in EPS revisions as Ned Davis’s ACWI EPS Revisions Indicator has turned up.

MARKETS

July’s equity outperformance was reversed in August with ACWI down over 4% led by EM down 6.5%, as LA fell 10%. Cyclicals led the way down in the US while global Value fell over 7%. Global Min Vol was a stud basically flat on a global basis. Equity funds saw big outflows during the month; Morgan Stanley notes that hedge fund exposure to Europe is as low as it has been since 2012 while Germany’s P/B discount to the US is at 18 yr wide & record wide vs rest of Europe as well. The EM Dividend space fell 8% as folks hiding out there picked up shop and left. EM equity outflows have been V significant.

In FI, the schoolyard bully fight continues with the duration bully winning the August round but taking it on the chin in September with 10 yr rates back up to 1.8%. It's important to note that fair value for the 10 yr UST is roughly 2% while 10 yr Bunds FV is considered roughly .13% or roughly 60 bps away from current levels. US IG continued to take in cash from abroad and rose over 3% for the month and is up over 15% ytd as issuance surges. US HY was flat for the month.

In Alts, Commodities took the lump of coal, down sharply for the 2nd month in a row as the energy complex cratered as did Base Metals. Silver & gold both had 7% up moves though silver still trails gold in YTD terms. Ag was down sharply given the trade wars, off 6% for the month and over 10% ytd. Volatility popped big time as SPY had numerous 1% move days - the VIX rose 23% for the month.

In the first two weeks of September the big story has been a massive factor rotation out of Momentum and Growth and into Value, by some accounts the most aggressive factor shift since 2009. This begs the question of whether we are at the beginning of the long awaited shift from Growth to Value and from US equity leadership to the Rest of the World which by sector makeup and valuation represents Value. Some are starting to suggest a generational type buying opportunity may be emerging in Global Value stocks. One hesitation concerns the capacity to have a regime change in a continued bull market; another is the need for economic growth to pick up for Value to work. History suggests that the current bull market needs to end with a recession and big equity selloff followed by a new growth phase and new equity leadership. (See Chart 4).

Chart 4: Factor Crash

Source: Tradingview

Could it be different this time? Instead of a recession perhaps we might have a continuation of our Lower for Longer Global Growth Path in which aggressive policy action in Europe and Asia contrasts with a US economy that is still in deceleration mode, allowing for global growth to rebound and the Value trade to start to work. Value has already priced in a recession - perhaps it's enough to not have one? The decision on generational change doesn't need to be made today but positioning for a Fall rally is more current business. Focus should be on non US equity exposure coupled with Cyclical sectors such as Energy, Financials and Industrials and Value Factors. Here it's worth noting that the average S&P return in the three months post a 2nd rate cut is roughly 10% appreciation.

It's clear that the factor reversal has been significant enough to really hurt some leveraged and trend following investors; time will tell how this affects the overall market. Note these same hedge funds and trend followers have been very long US equity, US rates and the USD relative to the rest of the world - thus any significant unwind could be an additional spur to non US equity performance. A trade deal/Brexit deal would also impact this discussion given how much these geo political issues have driven price action across multiple assets including commodities, FX and equity. For example, a trade deal could see the RMB trade back under 7 boosting EM FX while also boosting oil prices and base metals and potentially hammering gold and long duration USTs & Bunds.

PORTFOLIO STRATEGY AND ASSET ALLOCATION (GMMA)

We made several changes to our portfolios this month in an effort to lower portfolio volatility while maintaining our asset allocation. We remain overweight equities, underweight bonds, alternatives & cash.

While reducing our US equity underweight we remain overweight the non US equity markets with a focus on Europe and Japan given our belief that those markets offer greater room for appreciation based on ownership, valuation and currency upside. Should the shift to Value take hold both will benefit.

We slightly reduced our EM exposure which remains focused on China and Latin America; earnings growth, positive policy momentum in China & Brazil together with room for rate cuts in Mexico support those positions. A trade deal would propel China assets higher.

On a Factor basis, we increased our US Min Vol position, added a Global Min Vol position & maintained our US Value position.

In Fixed Income we reduced our duration underweight by adding to UST in the belly of the curve while eliminating our Mortgage Securities position.

We expect USD weakness based on Fed rate action, Presidential jawboning, massive twin deficits and a clear bottom in non US economic growth. The Euro screens very cheap relative to its history.

In the alternative space we exited our global miners position while adding a position in Silver. We continue to favor energy via our MLP position.

GLOBAL MACRO SUITE PORTFOLIO CHANGES

Global Macro Multi Asset (GMMA)

Within equities, we exited our Global Miners position & reduced our Asian EM position while initiating a Global Min Vol position and adding to our US Min Vol position.

Within the fixed Income sleeve we exited our US MBS position and added to our UST positions.

In the Alts sleeve we added a Silver position and reduced our cash position

Global Macro Income (GMI)

As in GMMA, we eliminated our US MBS position and added to our UST positions. Outside the US we consolidated our International Sovereign positions.

We added a Silver position which was funded from cash.

Global Macro Equity (GME)

As in our GMMA equity sleeve we exited our Global Miners position and reduced our Oil services position while adding a Global Min Vol position. We increased our US Min Vol position and added positions in US Healthcare and Cyber Security. We also reduced our Asian and China equity positions.

We hope you find this monthly piece of value and look forward to engaging with you on a monthly and quarterly basis as we go thru 2019.

Jay Pelosky, CIO & Co-Founder

TPW Investment Management

DISCLOSURE:

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. Returns can vary dramatically in separately managed accounts as such factors as point of entry, style range and varying execution costs at different broker/dealers can play a role. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts are inherently limited and should not be relied upon as an indicator of future results. There is no guarantee that these investment strategies will work under all market conditions, and each advisor should evaluate their ability to invest client funds for the long-term, especially during periods of downturn in the market. Some products/services may not be offered at certain broker/dealer firms.

There can be no assurance that the purchase of the securities in this portfolio will be profitable, either individually or in the aggregate, or that such purchases will be more profitable than alternative investments. Investment in any TPWIM Portfolios, or any other investment or investment strategy involves risk, including the loss of principal; and there is no guarantee that investment in TPWIM’s Portfolios, or any other investment strategy will be profitable for a client’s or prospective client’s portfolio. Investments in TPWIM’s Portfolios, or any other investment or investment strategy, are not deposits of a bank, savings and loan or credit union; are not issued by, guaranteed by, or obligations of a bank, savings and loan, or credit union; and are not insured or guaranteed by the FDIC, SIPC, NCUSIF or any other agency.

The investment descriptions and other information contained in this are based on data calculated by TPW Investment Management, LLC (TPWIM) and other sources including Bloomberg. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. This report should be read in conjunction with TPWIM’s Form ADV Part 2A and Client Service Agreement, all of which should be requested and carefully reviewed prior to investing.