As The Tri Polar World Turns - August 2019

MACRO THEMES

It's been a wild few months. June concluded what JPM called the broadest & strongest cross asset rally in a decade; July captured a “whiff of US exceptionalism” & resulted in strong US equity outperformance while the first week of August has upended the apple cart. To appreciate where one is, it helps to understand where one has been and hopefully the two allows one to construct an outline of a plausible future.

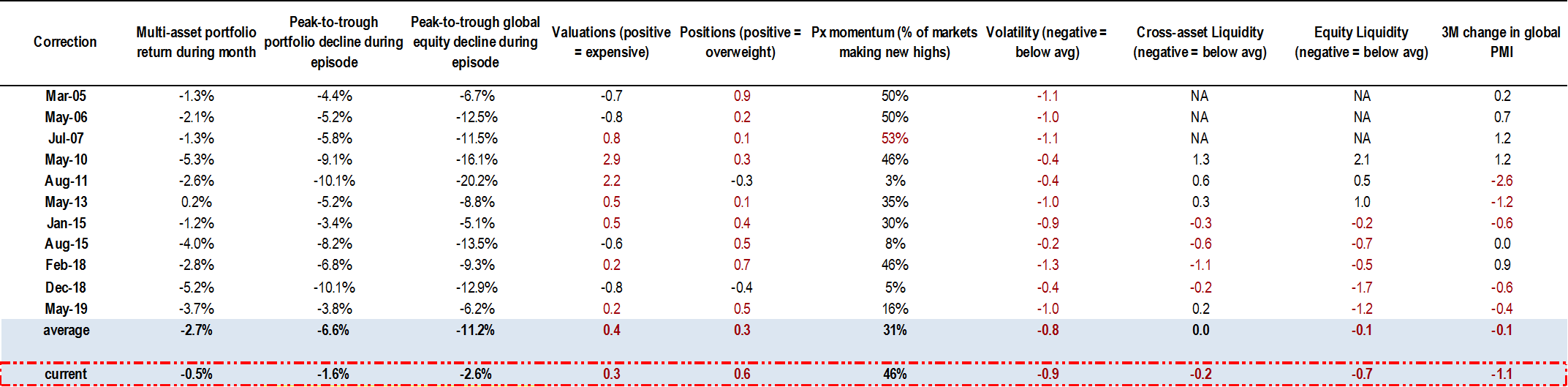

The tea leave reading seems quite tricky; the Fed’s first rate cut in a decade included either the Fed fumbling the rollout or the market misreading the presser while on the trade front, supposedly constructive meetings in Beijing were quickly replaced by Pres. Trump first announcing more tariffs before labeling China a currency manipulator. This combination sent equity markets into a tailspin, elongated a rip roaring global Govt bond rally and sent oil plummeting into a bear market (See Chart 1).

Chart 1: How Does Current Volatility Stack Up vs History?

Source: JPM, data as of 8/2/2019

What about the counterfactual? We have been focused first on our Lower for Longer Global Growth Path (DM decelerating to Potential Growth Rates and lower Neutral Rates of Interest = no US/EU recession) and second on our Big Four signposts for financial markets (Global Easing Cycle, Trade Front, Global Growth Bottom and EPS Outlook). As we held our monthly PM last week the Fed was about to cut, the trade front was quiet, global growth indicators were showing signs of life (GS Current Activity Indicators up M/M in July) and US/EU Q2 EPS were better than expected. A couple of tweets and the Yuan cracking 7 and it’s (seemingly) a different ball game. But is it?

That question is the one we need to answer as we go forward. To date, we believe it is not different and we are holding to our Lower For Longer Global Growth view. As for the Big Four, CB easing is broadening & accelerating - granted investors seem to be treating that as a confirmation of an imminent recession but that should change. The Trade Front is unlikely to deteriorate greatly from here (a very dangerous statement I know) as Trump has few options left and China is likely to focus on maintaining its economic growth path; Global growth may well be bottoming (note better China trade data) & earnings are likely to hold up as the gap between weak Manufacturing PMIs and stock market EPS has been one of the biggest takeaways from Q2 results.

We do worry that the uncertainty around trade could mean the growth bottom/recovery we expect might be shallower and bumpier than we have foreseen. We have previously noted the greater prospects for a risk asset melt up than a meltdown & see the early August sell off as akin to the May episode earlier this year and not the start of a Q4 2018 type pullback. Cross currents are everywhere and the tide is moving fast; we will remain vigilant and encourage you to do the same.

ECONOMICS

Amidst all the fire & fury, it's worth noting that in the latest IMF update the cut to global GDP growth was slight, from 3.3% to 3.2% for 2019 and from 3.6% to 3.5% for 2020. Both years are right in line with global growth post 2012 though well below pre GFC levels of 4%+. They are also well above global recession levels of 2.5%. Perhaps most interestingly, the 2019 EU growth forecast was left unchanged at 1.3%. As noted, Goldman’s CAI’s are picking up and showing month over month improvement while various data points from both Asia and Europe (SKorean IP, Taiwan Q2 GDP, Japan household spending, German factory orders, various European PMIs, China trade) suggest analysts may have become too negative in their growth outlook.

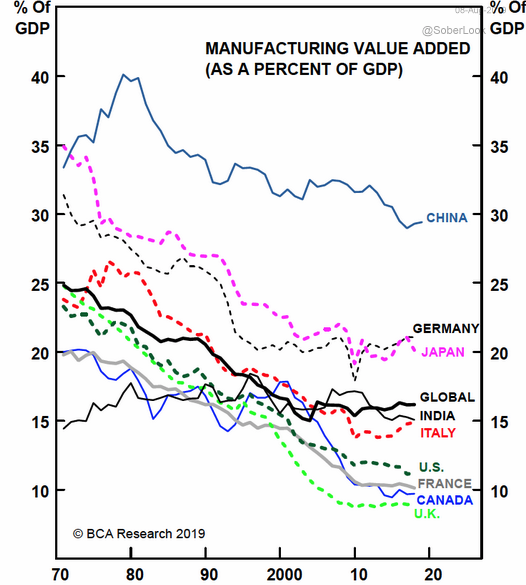

Q2 US GDP growth of 2% vs Q1 3% confirmed that the declaration we have discussed previously is now under way. Q3 is tracking at roughly 1.9% according to Ned Davis Research. We continue to believe the focus on Manufacturing PMIs is overdone as Services represent roughly 70% of DM economies (See Chart 2) & maintain our focus on the Composite PMIs, record low UER and rising wages across the DM economies. We did note that in the latest jobs report manufacturing hours worked were the lowest since 2011, which coupled with farm angst suggest much of Pres. Trump's support is under pressure. Both US Manufacturing and Service PMIs have rolled over suggesting continued slowing growth in the quarters ahead, which is likely to keep the Fed engaged.

Chart 2: Focus on Manufacturing PMIs is Overstated

Source: BCA, WSJ, United Nations and World Bank

Europe’s economy remains split between a very weak manufacturing cycle and a robust consumer/service sector. Germany, the region’s manufacturing powerhouse, has been particularly hard hit though recent factory orders picked up sharply, led by overseas orders. Hopes of German stimulus have been raised, rebuffed by the Minister of Finance and raised again. Germany’s economy is now the 2nd weakest in Europe; its large budget surpluses, imploding banking system and massive trade surplus (a juicy target for Trump) suggest some fiscal stimulus is possible (Q2 GDP next week is likely to be negative). At the moment, negative rates in Germany & throughout Europe are seen as a sign of how bad things are rather than as an opportunity to borrow and build.

In Asia, China continues to move along a bottoming path or L shaped recovery. US - China trade continues to migrate away from China to the rest of Asia boosting Asian integration & reflecting how the trade conflict is accelerating our Tri Polar World construct. Recent GS research suggests that the Asian trade cycle should begin to bottom soon; the current slowdown has been longer than usual & exports are undershooting trade partners activity levels. Several Firms are also calling the bottom in the semi cycle due to sharp production cuts and inventory work downs. Asian Central Banks are also actively cutting rates with New Zealand, India and Thailand all cutting rates just this week.

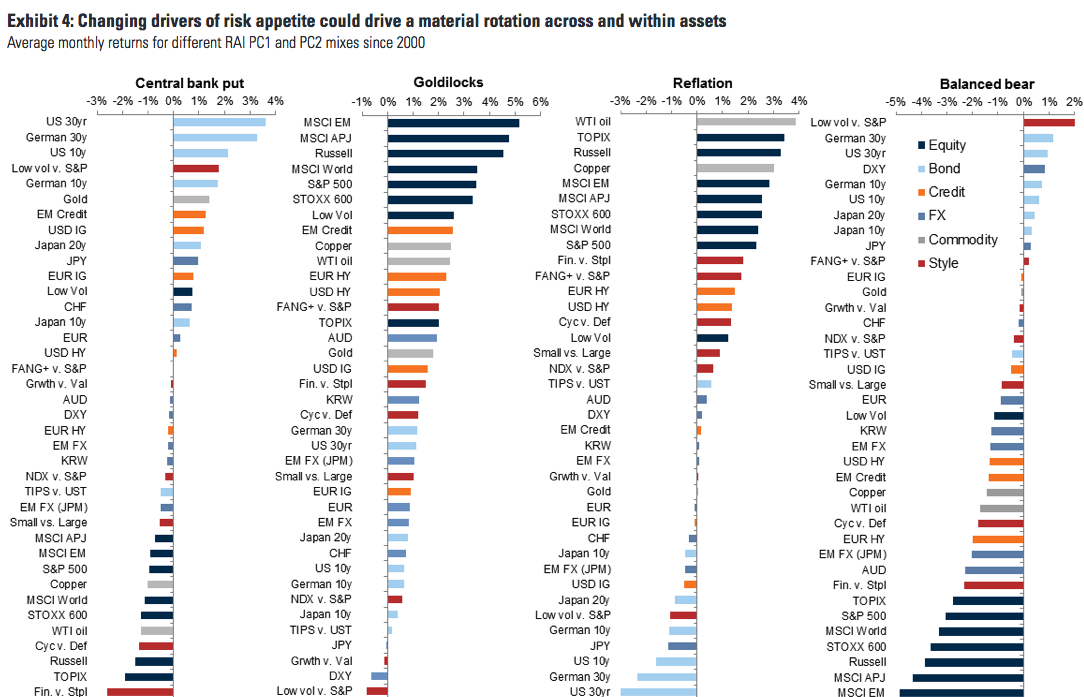

Goldman Sachs expects how the 2nd H of 2019 plays out will depend on the interaction between monetary policy and global growth & sees 4 possible scenarios (See Chart 3): CB put (weak growth, more easing); Goldilocks (easing & better growth); Reflation (growth & rising rates) and Balanced Bear (tight money & weak growth). Goldman looks for split between #3 and 4 in 2H; we expect more of a combo of #1-2, CB easing together with growth bottoming & picking up.

Chart 3: Four Scenarios for 2019’s 2nd Half

Source: Datastream, Haver Analytics, Goldman Sachs Global Investment Research

POLITICS

The US Presidential campaign is well underway and it's clear that Pres. Trump will play to his base while Democrats play to theirs. The debt ceiling/budget agreement suggests the basic work of Govt can still get done, a positive surprise. Our expectation that Trump would remain conventional on the world stage while bombastic on the campaign trail has been called into question on both fronts: on the global stage with his tariff/ currency & Fed tweets & domestically by the multiple mass murders in the US. Arguably the President is becoming what we used to call a “multiple contractor”, limiting risk asset upside by raising the uncertainty level. As JPM has noted, in the three trading days post Trump’s tariff tweet the S&P dropped 8% intraday and global equities shed over $5T or roughly 170x the $30B collected to date in tariffs. That’s not a great P/L.

After a period where investing on macro fears seemed to guarantee poor performance (Brexit, Trade) it has once again become the thing to pay most attention to. That doesn't seem right to us and we expect once the furor dies down that the focus will return to economic policy and corporate results. One key to watch is whether US - China trade talks set for September in DC will take place. Most recent reports suggest they will. Hopes for any positive momentum at this point are at a low, suggesting possible upside. Both sides are narrowing down to a dispute over beans (Agriculture) for bits (Huawei); counterintuitively this suggests a deal could get done.

Europe has finished the horse trading around its top jobs - we will see how the new leadership performs with a focus on fiscal stimulus to go along with renewed monetary easing by the ECB. Brexit has risen back to the top of the EU political calendar with new PM Boris Johnson coming out with hard Brexit guns blazing and sterling tumbling in response. Most banks still see such an outcome as having less than 30% chance.

In Japan, Upper House election success by PM Abe’s party suggests the October VAT hike will take place as strong spending data suggests the pull forward of consumption may have begun. The Japan - SK trade fight remains a worry while India’s Kashmir decision raises the political temperature there as well. The China - HK dispute could also turn problematic; China’s top leadership is on a two week internal conclave; we will have to wait to see if any policy changes come about as a result. The G7 Summit is at the end of the month - things are so hectic no one is even talking about it yet.

POLICY

The shift from Powell pivot to Powell put is complete though Chair Powell continues to find the speaking part of his job very tough. He is not alone as Chair Draghi also failed to impress with his press conf, noting a “worse and worse” outlook but not doing anything about it. As the main CB’s join the global easing cycle rather than providing an underpinning for risk asset pricing they appear to be stimulating more fear about the global growth cycle. This seems a little perverse.

We expect the Fed to continue to ease but in an insurance cut fashion. The annual Jackson Hole meet later this month may shed more light on the Fed’s approach. We expect the ECB to act in September but in the interim the market is doing it for them with BUND yields at -.60% and negative yielding debt piling up week by week. We expect a full throated global easing cycle to continue as more countries realize the need to stimulate their own demand - the good news is room exists to do so post last year’s EMFX fears. As an example, Brazil has cut rates to record lows while Mexico is likely to cut as it now has the 2nd highest real rates in the world behind only the Ukraine.

Trade policy seems to be a wild card; we were surprised that Pres. Trump added a 10% tariff to the remaining $300B of Chinese exports and even more surprised that the US labeled China a currency manipulator. Going forward we do not expect a 2015 style Chinese devaluation process believing that China learned many lessons from that episode. It does seem that more tariffs could lead to a weaker Yuan with several Banks noting a Full Monty tariff structure (25% on the full $500B of exports) would require a Yuan rate at 7.70 to fully offset the tariffs.

We don't expect the Full Monty to be put in place and see recent risk asset volatility as almost ensuring such given the downside to risk asset pricing (tech shares especially), household net worth, consumption, the US economy & thus the President’s reelection prospects. One benefit of the recent market volatility is that policy makers are now on full alert.

MARKETS

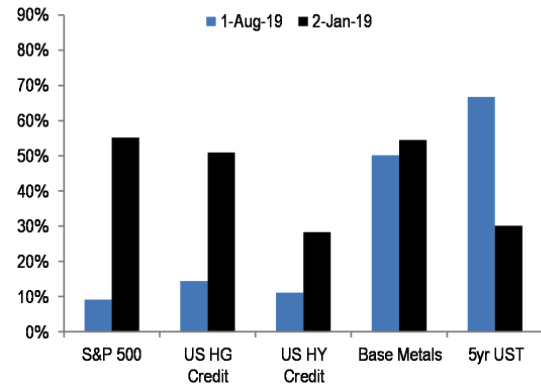

In the first week of August risk assets have sold off sharply with equities selling off as a group led by EM, now at 15 yr lows vs ACWI. Govt bonds rallied sharply, seemingly signaling an impending recession. It's worth noting that bonds don't always get it right - see 2016-17 for the most recent example. Chart 4 shows how different assets have priced recession risk in different periods. Commodities have been very weak, led by oil, off roughly ~10% in a month (7% in one day) and entering a bear market - watch the early Sept OPEC + meeting. Base metals and Ag also sold off sharply given China’s decision to stop buying US Ag products in retaliation for the US adding tariffs. The USD, which had been threatening to break out to the upside instead has reversed as the UST rally shrunk the yield premium vs the rest of the world, leading to USD weakness especially against the Euro while the Yen benefits from safe haven status.

Chart 4: Both Stocks and Bonds Can’t be Right About Recession Risk

(Chart shows probability of US recession priced in across asset classes)

Source: JPM

There have been many cross currents to note; within FI the credit spread between UST and HY has widened out to a pretty juicy 450 bps. Given the oil selloff, HY has held in well and importantly is not supporting the UST recession signal. We continue to think the market structure of machine driven trading is exacerbating market moves and potentially sending incorrect signals regarding the state of the real economy both in the US and globally. Fixed Income has a school yard bully problem: either one has to fight the duration bully or the Fed/Global CB bully who has a buddy named China stimulus. Equities are watching and hoping that the Fed bully wins, steepens the yield curve and stimulates growth.

At this point growth plays are deeply oversold while safety assets are deeply overbought. The US equity market has switched from quite overbought to oversold according to Ned Davis Research. While August through Sept is seasonally weak for equities, it's important to note that August is the strongest buyback month of the year in the US while buybacks have expanded in both Europe (record over past one yr) and Japan. It's also important to note that as bond yields have collapsed the case for equity valuation becomes stronger while most equity markets are flat to down slightly on a 12 month trailing basis. JPM reports that the S&P earnings yield is close to 6% while global Govt bonds yield 0.6%, putting the spread between the two at over 5%, one of the most attractive since 1985. In addition Q2 US EPS are up 4% y/y and up from the 2% y/y gain in Q1, suggesting not an earnings recession but earnings acceleration albeit modest. EPS has come in better than forecast in Europe as well.

While perhaps hard to imagine today, the upcoming months could bring a preponderance of data that global growth & earnings are indeed bottoming, that Central Banks will continue to support the economy, that the trade front will go quiet and that the world is not about to enter a “currency war”. If so, the prospects for equity markets to move back to recent highs and above in the case of the non US markets seems quite viable. The changes to market leadership, from the US to ROW, from Growth to Value and from Defensives to Cyclicals remain possible as does the shift from Govt debt to Credit and from the USD to other currencies while Commodities, now priced back at 2016 lows, would likely move appreciably higher.

PORTFOLIO STRATEGY AND ASSET ALLOCATION (GMMA)

We made very few changes to our portfolios this month; as such we remain overweight equities, underweight bonds, alternatives & cash.

We remain overweight the non US equity markets with a focus on Europe and Japan given our belief that those markets offer greater room for appreciation based on ownership, valuation and currency upside. Japan in particular screens as very cheap relative to its history.

Our EM equity exposure remains focused on China and Latin America; earnings growth, positive policy momentum in China & Brazil together with room for rate cuts in Mexico support those positions.

In the US, we are focused on cyclical plays (transports, energy, and value) balanced with defensive positioning (min vol) as we gain exposure to an anticipated global growth bottom. While underweight Tech, we do like the software space as being insulated from Tech Splinternet, Trade tiffs, and benefitting from the corporate search for efficiency.

In Fixed Income we remain underweight duration and overweight credit, both in the US and abroad. We continue to prefer EM $ debt which screens very cheap relative to its history - one of the very few FI instruments to do so. Preferred securities, US HY also remain favorites.

We expect 2nd Half USD weakness based on Fed rate action, Presidential jawboning, massive twin deficits and a clear bottom in non US economic growth. The Euro screens very cheap relative to its history.

In the alternative space we continue to favor energy via our MLP position together with the miners which we expect to be among the winners in a growth pick up scenario.

GLOBAL MACRO SUITE PORTFOLIO CHANGES

Global Macro Multi Asset (GMMA)

Within equities, we have exited our US High Dividend position and replaced it with a US Value focused position as we further shift our portfolio positioning to gain exposure to an anticipated global growth bottom.

Global Macro Income (GMI)

No changes this month

Global Macro Equity (GME)

As in our GMMA equity sleeve we reduced our US High Dividend position and added a US Value position.

We hope you find this monthly piece of value and look forward to engaging with you on a monthly and quarterly basis as we go thru 2019.

Jay Pelosky, CIO & Co-Founder

TPW Investment Management

DISCLOSURE:

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. Returns can vary dramatically in separately managed accounts as such factors as point of entry, style range and varying execution costs at different broker/dealers can play a role. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts are inherently limited and should not be relied upon as an indicator of future results. There is no guarantee that these investment strategies will work under all market conditions, and each advisor should evaluate their ability to invest client funds for the long-term, especially during periods of downturn in the market. Some products/services may not be offered at certain broker/dealer firms.

There can be no assurance that the purchase of the securities in this portfolio will be profitable, either individually or in the aggregate, or that such purchases will be more profitable than alternative investments. Investment in any TPWIM Portfolios, or any other investment or investment strategy involves risk, including the loss of principal; and there is no guarantee that investment in TPWIM’s Portfolios, or any other investment strategy will be profitable for a client’s or prospective client’s portfolio. Investments in TPWIM’s Portfolios, or any other investment or investment strategy, are not deposits of a bank, savings and loan or credit union; are not issued by, guaranteed by, or obligations of a bank, savings and loan, or credit union; and are not insured or guaranteed by the FDIC, SIPC, NCUSIF or any other agency.

The investment descriptions and other information contained in this are based on data calculated by TPW Investment Management, LLC (TPWIM) and other sources including Bloomberg. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. This report should be read in conjunction with TPWIM’s Form ADV Part 2A and Client Service Agreement, all of which should be requested and carefully reviewed prior to investing.