As The Tri Polar World Turns - 2nd Half 2020 Outlook "The Great Reopening"

MACRO THEMES

Speed is the signature of the Covid-19 era and so to keep pace we have sped up our 2H 2020 Outlook to mid-May. We remain constructive on risk assets and expect continued global policy support, economic bottoms, zero rates, gradual reopenings, bearish & underweight investors & scientific advancements to lead risk assets higher. The current pullback provides an entry opportunity. Downside risks remain centered around renewed virus outbreaks sufficient to require economy wide lockdowns together with growing political risk centered around the US presidential election cycle and perhaps manifesting in further escalation of US - China tensions.

The one area where Covid-19 has not overturned the existing order is in US, tech led, global equity leadership. The chaotic nature of the US reopening process may facilitate a change in that dynamic. We continue to focus our attention on two key questions: first, the potential for new equity leadership to emerge from the bear market/global recession and second the potential for the Reflation 2020 case we laid out last December to resurface late this year and into 2021-2022. We see the two as linked & increasingly likely - we explore below.

HEALTH

Investing in the Covid Age means leading off with health. The good news is that confirmed infection case growth rates are declining in most countries with several having all but stamped out the disease (though perhaps for only the time being). More encouraging still is the Asian/European reopening process that has proceeded with very little in the way of renewed outbreaks. Isolated clusters yes, large scale outbreaks no - that distinction will be key going forward, as will the testing & tracing regimes to ensure it remains so.

China, for example, has told its people to no longer wear masks outdoors while reopening large crowd events such as Shanghai Disney. It is now assessing the outbreak risk from the country’s May Day holiday which featured over 100M domestic tourist trips. China emerging from May Day outbreak free would send a strong positive signal to the ROW in the Covid-19 global reopening queue.

This last point, that there is a reopening queue, seems critical. Staying safe by following in the footsteps of the one ahead is something I learned climbing in the High Himalayas back in the day. The US in particular has the benefit of following in the footsteps of not only China or S Korea but also Germany, Denmark, Austria and others. This is true for policy makers, companies & individuals as well. With European factories & schools reopening, sports resuming and restaurants once again offering a chance to dine in, the US can learn much from those ahead of it.

Worryingly, the US seems resistant to this learning. With 40 states now in some stage of reopening, the US reopening process is consistent with its chaotic approach to the virus to date. The Trump Admin continues with a hands off approach to much of the blocking & tackling of the virus, from equipment acquisition (PPE) to lockdowns, testing and now reopenings. The disagreement between Pres. Trump & Dr. Fauci over the outlook is just the latest example.

Thus the US reopening seems to be the most risky given that the national case curve remains more of a plateau than a steep decline with roughly 20k new cases per day. This suggests relying on China et al for guidance should be taken with a grain of salt given the notably different US set up going into the reopening process. US testing levels, while much improved, still stand at roughly 50% of what is recommended while the tracing system, so important to ensure localized outbreaks don’t mushroom, remains virtually nonexistent at the national level.

As a New Yorker I can say that NYC’s response to the lockdown has been even more impressive than I expected - it would be a real shame if all that effort (and economic cost), designed to protect the healthcare systems & allow the Govt to catch up to the speed of the virus, were to be for naught. (See Chart 1).

Chart 1: US Reopening Risky Given Lack of Test & Trace Capacity

Source: Pantheon

ECONOMICS

The data has been and remains quite dismal, in sharp contrast to positive risk asset performance, thus providing plenty of media fodder. To us, it's quite simple - markets are forward looking & data is backward looking. Covid-19’s signature, its speed, has meant that economic bad news is front loaded, unlike traditional recessions where the bad news gradually builds. We have seen this in the US jobless claims and the April jobs report with its 14% UER. The rapid peak and decline in jobless claims suggest that while May’s UER may be even higher than April, it may mark the peak for this cycle. Stunning and scary as it is, the Covid recession is likely to be short lived as well.

The shape of economic recovery remains an open question; the betting is more U or W shaped (roughly 75% of a recent BofA survey). Given only 15% bet on a V that tells one where the upside lies. Much depends on the success of the reopening. A few months into its reopening & China’s economy seems almost fully back on the production side and rapidly improving on the demand side. April IP was up almost 4% y/y, car sales were also up y/y while the Shanghai Disney tickets for reopening were sold out in minutes. US/EU Q1 company reports add further insight to China’s economic recovery path.

Going forward, we plan to pay close attention to the demand side of the picture. Advanced economies are 70%+ consumption so economic recovery will really boil down to how safe consumers feel going out, shopping, dining, attending sporting events etc. This is where the intersection of health and economics meet & it is the most worrisome aspect of the US reopening. If the testing and tracing regime is not robust enough to convey a sense that it is safe to move about, then reopenings will be slow and disjointed. If the comfort level is there then we expect demand to follow given the tremendous global liquidity that is being provided on a synchronized basis across the globe. Further support stems from US consumer savings at 13% of GDP marking a 39 yr high while US IG debt issuance has been off the charts over the past six weeks or so. (See Chart 2).

Chart 2: Global Liquidity Support Underpins Economies & Markets

Source: JPM

Could all this liquidity lead to reflation? While Covid-19’s immediate economic thrust is clearly deflationary, the global policy response, oil/commodity bottom, product shortages and the risk of supply chain interruption suggest there could be more of a reflationary lift than currently expected. It's more a when than if question; by late 2020 or 2021 we expect a more consistent inflationary path. Massive debt levels may also spur arguments to inflate away the debts. (See Chart 3)

Chart 3: Will Covid-19 Drive a Regime Shift from Disinflation to Reflation?

Source: BofA, Bloomberg, Haver

POLITICS

US - China relations are back front and center as the Trump Admin seeks to both deflect from its own failings while making the electoral case that it can best keep America safe from a rising China. For its part, China appears to have overplayed its post Covid-19 hand, at least insofar as Europe is concerned.

Viewed through our Tri Polar World (TPW) prism it's clear that the three poles: Asia, led by China, Europe and the Americas, led, such as it is, by the US, are positioning themselves for the recovery. While fights over AI and climate recede into the background, the fight over who gets a vaccine first and how it will be distributed takes center stage. The failure of the US to join in broad, multinational efforts to fund vaccine research stands out in this regard.

Europe is focused internally on several fronts: the restart of EU- UK Brexit talks, the funding of a joint recovery effort & a court battle over the ECB’s post GFC policy mix. The German constitutional court’s decision regarding the legality of ECB bond buying efforts & its suggestion that the Bundesbank might have to excuse itself from such efforts is extremely problematic. A solution is likely to be found (because one has to be) but with a three month window to do so Germany’s political leaders need to act fast; the timing couldn't be much worse as it reminds one and all that Europe will seemingly choose to shoot itself in the foot whenever it gets the chance.

The Americas have not been faring any better. Mexico struggles to get a grip on the virus, Argentina prepares for yet another debt default, Brazil’s political class reopens its internal wars while the US struggles to deal with Covid-19, a patchwork reopening and a cross spectrum of ills revealed by the virus ranging from healthcare, to labor policies, to who gets what piece of Governmental assistance.

President Trump is desperate to reopen the economy and put the daily death toll behind him but risks all in his approach. With WH staff now coming down with the virus, new case counts totaling roughly 20k per day and the death toll likely to reach 100,000 by Memorial Day it is not a pretty picture for the incumbent. We expect the election to turn on who the electorate sees as a safe pair of hands. Growing talk of a Democratic sweep (House, Senate, Presidency) & prospects for tax hikes to follow is already expressed in the VIX forward curve while a quick glance at how taxes rose from 1929-39 provide historical precedent. We don’t expect US - China relations to deteriorate significantly; plenty of smoke, yes, especially from the US side, but no real fire. Neither side can afford further economic weakness beyond that imposed by the fight against the virus.

POLICY

Policy, especially Central Bank policy, has been the hero of the Covid Age. Prompt, aggressive and unprecedented activity by the Fed, BOE & others short circuited many of the worst fears expressed in the depths of the selloff. Without spending a single dollar Chair Powell stabilized the credit markets, putting Mario Draghi’s famed whatever it takes speech in the shade.

Fiscal policy also has been brought to bear in many countries creating an unprecedented amount of stimulus that to date has supported risk appetites, stabilized markets & protected workers/businesses while setting the stage for robust recovery should the science allow it. Distinct regional differences in labor policies have been revealing: limited pick up in Asian UERs, broad European application of Germany’s Kurzarbeit worker furlough program contrasting with US policy of mass layoffs and 14% UER (the US went from roughly half Europe’s UER to double it in less than 3 months). Labor has been and will remain at the forefront of concerns given the importance of consumption to overall economic growth. (See Chart 4)

Chart 4: Rolling Thunder of Policy Responses Support Financial Markets

Source: Alpine Macro

There is also health & science policy to consider. Speed has been Covid-19’s calling card; might it also apply to the speed in which the global science - tech community identifies a solution to the virus? This community’s unprecedented focus on Covid-19 suggests that betting against science in this instance may be wrong headed. In essence being bearish implies one is betting against not only the Fed & global policy response but also the global science & tech community.

Covid-19 continues to deepen the regional integration that underpins our TPW view. Witness the discussions between China and S Korea to reopen trade & the “tourist bubble” between Australia and New Zealand. Europe, very exposed to tourism & hospitality itself, is planning to reopen land borders by mid-June. In the Americas we have supply chain issues confronting Mexico, the US and Canada, especially in the auto sector. How cross border trade restarts will have big implications for national, regional and global growth.

As countries reopen, the Rolling Thunder of policy responses continues. Just this week India announced a stimulus program worth 10% of GDP, Italy announced a $60B program and the US House prepped a $3T Phase 4 bill. We expect Phase 4 to be approved; it's an election year after all. Expect more policy action in China post its upcoming National Congress meeting; it's kept much of its policy powder dry. In Europe there is the potential for a joint recovery plan funded by an enlarged EU budget and focused on fleshing out the Green Deal. One of the risks of a 2nd wave in the Fall or renewed lockdowns is the potential for stimulus fatigue as policy makers start to worry about budget deficits (likely to be record levels across the globe), currency risk and potential inflation concerns. Such concerns appear to be partly responsible for recent risk asset weakness.

MARKETS

One area Covid-19 has not yet been able to upend is the tech led US equity leadership. With the FANG+ stocks up over 15% ytd and Q1 US outperformance the song remains the same. Will it continue that way? There are early signs that those countries who have successfully reopened, mainly in Asia but also some European countries, are starting to outperform. The US reopening process is inherently more risky than others because of its failure to put in the work on testing & tracing. In contrast, much of Asia has done that work (China, SKorea, Taiwan) is first out of lockdown, tech centric with much lower unemployment, more dry policy powder, & is a big beneficiary of low oil prices.

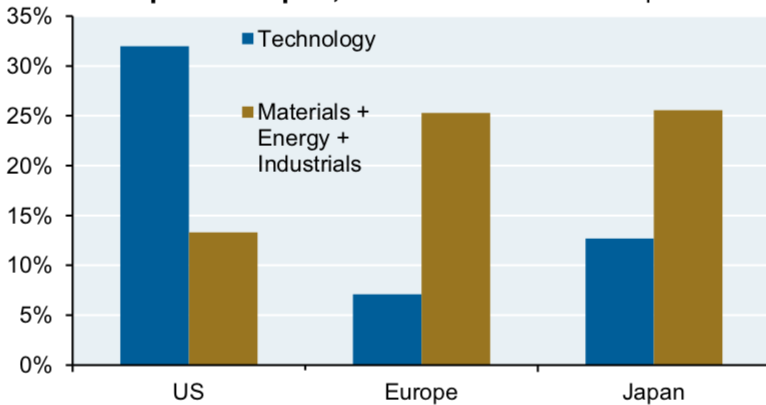

As economies recover history suggests Small Caps & Cyclicals should do well. While it's clear that Tech has led and that the new phase of Work From Home (WFH) suggests digitalization will advance further & faster than expected, it's also the case that the broad market remains where the value lies with the median US/EU stock still roughly 30% off its highs. Tech stocks have been huge winners from the collapse in long rates - that prop may pop. There is scope to make the case that economic recovery will bring about new leadership, helping to broaden the market's advance & sustain a run to new ATHs over the coming 12 months. A broader market advance is a healthier market advance. (See Chart 5)

Chart 5: Tech – Cyclical/Value Barbell

Source: Bloomberg, 5.10.2020

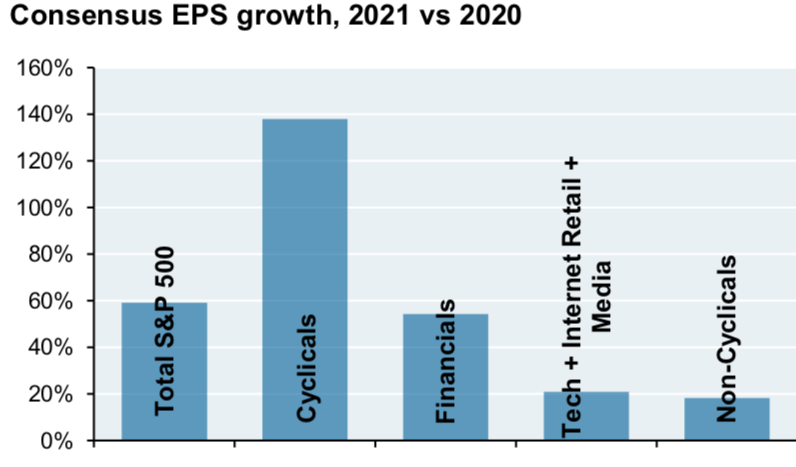

We think there is a reasonable chance that as economies recover, rates will back up supporting Financials, a big part of the Value & Cyclical segments while Industrials, Energy and other left behind sectors can start to perform. We noted in a recent Musings (link) that the bond market may be the “tell” for equities. A further steepening of the yield curve seems likely, as the Fed pins the short end while the long end rises to reflect economic recovery, huge long dated supply and potential inflation risk. Granted the near term outlook seems dim for inflation but this to be expected when quarterly GDP is plummeting; what happens when GDP spikes back up? (See Chart 6)

Chart 6: Cyclical Earnings Spike in the Year Ahead

Source: Bloomberg, 5.10.2020

We believe the old saw: Sell in May & go away will prove misguided this year. Risk assets may surprise over the summer on continued policy support & successful reopenings before pulling back and awaiting Fall 2nd wave risk together with US electoral uncertainty. Speed on the science side is a wildcard. BofA notes its private clients hold 14% cash while it’s Bull/Bear indicator remains stuck at zero - uber bearish. This week several well-known investors called the US equity market massively overvalued which coupled with dour tones from both Health (Dr. Fauci) and Fed chair Powell, have fueled a 5% pullback.

We would look to buy the dip & note that valuation is not a great NT indicator while the US & tech has been expensive for years, especially on a relative basis. The S&P trades at roughly 17x 2021 bottoms up estimates, in line with recent history. (See Chart 7)

Chart 7: Bearish & Underweight Investors Provide Upside Fuel

Source: JPM

PORTFOLIO STRATEGY AND ASSET ALLOCATION (GMMA)

We maintain an equity overweight implemented via a barbell strategy with tech and Value-Cyclical sectors anchoring the two ends. We think current small cap weakness presents an opportunity and have built positions in biotech, recognizing that the health sector will play an outsized role in any true recovery. Stocks offer growth with yield in a yield starved global investment landscape. We have moved to a more neutral regional positioning, recognizing the importance of US tech and the limited nature of Europe’s stimulus to date. We continue to favor Asia, including both Japan & China, as the first region in & out of Covid-19 lockdown. We remain cautious on EM equity which while setting new lows vs the US also bears significant concerns especially in LatAm, Turkey, etc.

Within a fixed income underweight position we favor credit, backstopped by Central Banks & supported by a continued Search for Yield evident in the huge demand for long dated US IG debt & peripheral European sovereign issues. With investors OW IG by the most in three years, we favor HY within the credit space and believe that the default cycle will be less worrisome than many forecast. We continue to like Preferreds, EM USD debt and TIPs. We hold a small cash position.

FX land has been and remains quite quiet. We have noted that costs to short the USD have declined back to 2015 levels suggesting some USD downside risk. EMFX has stabilized notwithstanding worries from Turkey to Brazil and points in between. Until the ROW starts to accelerate its growth pickup FX vol is likely to remain muted. We are watching the A$/Y cross as a global growth signal… so far it looks constructive.

We have also built a neutral position in the commodity space which remains unique among the asset classes for not having recovered to any meaningful extent. We noted some weeks back that the oil price collapse represented the third and last shoe to drop thus marking the commodity bottom. As economic activity picks up, demand for industrial metals and energy should do the same. We continue to have a sizable gold position across both the metal and the miners and expect gold to perform well in most forward scenarios.

I hope you find this monthly piece of value and look forward to engaging with you on a monthly basis as we move through 2020.

Jay Pelosky, CIO & Co-Founder

TPW Investment Management

DISCLOSURE:

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. Returns can vary dramatically in separately managed accounts as such factors as point of entry, style range and varying execution costs at different broker/dealers can play a role. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts are inherently limited and should not be relied upon as an indicator of future results. There is no guarantee that these investment strategies will work under all market conditions, and each advisor should evaluate their ability to invest client funds for the long-term, especially during periods of downturn in the market. Some products/services may not be offered at certain broker/dealer firms.

There can be no assurance that the purchase of the securities in this portfolio will be profitable, either individually or in the aggregate, or that such purchases will be more profitable than alternative investments. Investment in any TPWIM Portfolios, or any other investment or investment strategy involves risk, including the loss of principal; and there is no guarantee that investment in TPWIM’s Portfolios, or any other investment strategy will be profitable for a client’s or prospective client’s portfolio. Investments in TPWIM’s Portfolios, or any other investment or investment strategy, are not deposits of a bank, savings and loan or credit union; are not issued by, guaranteed by, or obligations of a bank, savings and loan, or credit union; and are not insured or guaranteed by the FDIC, SIPC, NCUSIF or any other agency.

The investment descriptions and other information contained in this are based on data calculated by TPW Investment Management, LLC (TPWIM) and other sources including Bloomberg. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. This report should be read in conjunction with TPWIM’s Form ADV Part 2A and Client Service Agreement, all of which should be requested and carefully reviewed prior to investing.